🏠 Introduction

Buying a new house? Starting 01 April 2026, the Income Tax Department has introduced Form 141 as a consolidated challan-cum-statement for TDS reporting. This replaces Form 26QB, which was earlier applicable for property transactions. Now, all PAN-based TDS reporting is streamlined under Form 141.

📄 What is Form 141?

- Form 141 is a unified challan-cum-statement introduced under the Income Tax Act, 2025.

- If agreement/ payment date is on or before 31st March, 2026, old Form 26QB is applicable. Form 141 is applicable for transaction date on or after 01st April, 2026.

- It consolidates earlier forms (26QB, 26QC, 26QD, 26QE).

- It has following annexures:

- Schedule A: TDS on rent paid by an Individual/HUF

- Schedule B: TDS on transfer of immovable property

- Schedule C: TDS on payments made by an Individual/HUF to contractors or professionals

- Schedule D: TDS on transfer of Virtual Digital Assets (VDA) by an Individual/HUF

- For property transactions, Schedule B of Form 141 applies.

- It must be filed online via PAN login on the e-filing portal.

- Applicable only for resident deductees.

🆕 Key Updates in Form 141

- Single Buyer, Multiple Sellers – One Form

- If there is one buyer and multiple sellers, only one Form 141 needs to be filed.

- However, if there are multiple buyers, then separate Form 141 filings are required for each buyer.

- Proportion of Agreement Value

- The buyer must specify the proportion of agreement value attributable to each seller.

- This ensures clarity in reporting and accurate allocation of TDS liability.

- Instalment-Based Payments

- Where property consideration is paid in instalments, details of previous Form 141 filings for earlier instalments must be provided.

- This creates a linked compliance trail and prevents duplication or omission of TDS entries.

📅 Applicability

- Effective Date: 01 April 2026

- Applicable From: FY 2026-27 onwards

- Scope: Deduction of TDS on transfer of immovable property under Section 393(1).

- Threshold: TDS applies if property value exceeds ₹50 lakh.

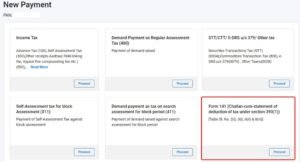

🛠️ Steps for Filing Form 141 (Schedule B)

- Login to the e-filing portal with PAN credentials.

- Navigate to e-File → e-Pay Tax → Income Tax Act, 2025 → New Payment → Form 141.

- Single Buyer, Multiple Sellers – One Form

3. Select Schedule B:

4. Select Deductee Type (Corporate/Non-Corporate).

5.Enter Deductor details (auto-populated from profile).

6.Fill Transaction Details:

-

- Type of property (Land/Building)

- Address of property

- Date of agreement & registration

- Stamp duty value & consideration amount

- Mode of payment (lump sum/instalments)

- Details of all buyers (PAN, share %)

- Details of all sellers (PAN, share %)

7. Enter TDS details (auto-calculated based on transaction).

7. Enter TDS details (auto-calculated based on transaction).

8.Preview, confirm, and make payment via bank portal.

9.Download Challan Receipt for records.

🔄 Key Changes: Form 26QB vs Form 141 (Schedule B)

| Aspect | Form 26QB | Form 141 (Schedule B) |

| Applicability | Only property transactions | Consolidated across property, rent, contractors, VDA |

| Effective FY | Till FY 2025-26 | From FY 2026-27 |

| Filing Mode | Separate form for each transaction | Unified portal tile, schedule-based |

| Multiple Deductees | Limited handling | Allows multiple deductees of same type |

| Validation | Basic checks | Enhanced validations (stamp duty, instalments, PAN type) |

| Law Reference | Section 194-IA | Section 393(1) under IT Act, 2025 |

✅ Conclusion

With Form 141 (Schedule B), property buyers must adapt to a new unified TDS reporting system from FY 2026-27. While the filing process is similar to 26QB, the new form offers better validations, consolidated reporting, and simplified compliance. Buyers should ensure they are familiar with the updated steps to avoid penalties and maintain smooth compliance.

Blog By : Mittal & Co.