Advance Tax Calculation FY 2025-26 (AY 2026-27) – Things to Remember!

Introduction Advance tax is one of the most important compliance requirements under the Income Tax Act. It ensures that taxpayers pay their dues in instalments as income is earned, rather than waiting until the end of the financial year. This “pay-as-you-earn” system prevents a heavy burden at year-end and helps the government maintain steady revenue […]

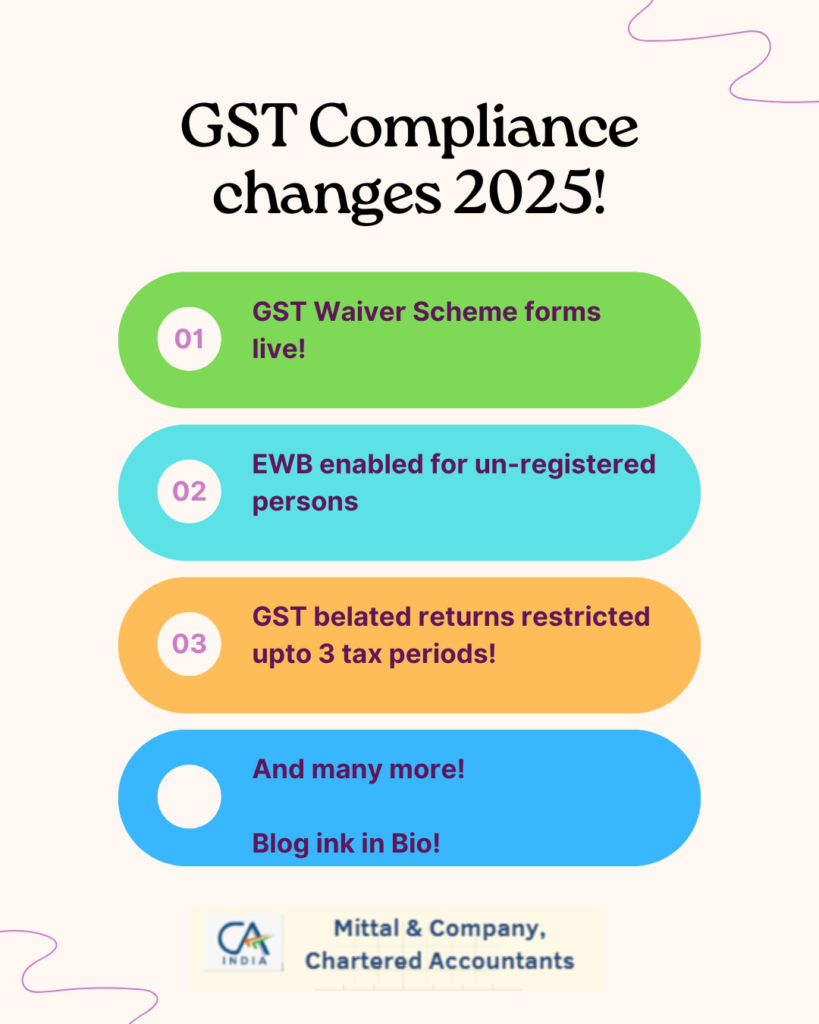

GST Update: Withdrawal from Rule 14A from 21 Feb 2026

Introduction On February 21, 2026, GSTN rolled out a new online facility allowing taxpayers to withdraw from the option availed under Rule 14A of the CGST Rules. This is a significant compliance update, as it provides clarity and a structured process for opting out through the filing of Form GST REG-32 on the GST Portal. […]

Income Tax & Surcharge Rates for FY 2025-26 (AY 2026-27)

Income Tax & Surcharge Rates for FY 2025-26 (AY 2026-27) Income tax planning requires a clear understanding of applicable tax rates, surcharge slabs, and rebates. For FY 2025-26 (AY 2026-27), taxpayers can choose between the old regime with exemptions and deductions, or the new regime with simplified slabs and higher exemption limits. Below is a […]

Income Tax Act 2026: Complete Form Number Changes

Introduction: The transition from the Income Tax Act, 1961 to the Income Tax Act, 2026 has brought significant structural and procedural changes, including comprehensive renumbering, consolidation, and rationalisation of statutory forms. While the core compliance framework such as audit reports, TDS/TCS statements, certificates, declarations, and applications continues in substance, the form numbers and corresponding section […]

Budget 2026: What It Means for MSMEs in India

Introduction The Union Budget 2026–27, presented by Finance Minister Nirmala Sitharaman, has once again placed Micro, Small, and Medium Enterprises (MSMEs) at the center of India’s economic growth narrative. MSMEs are vital engines of employment, exports, and supply-chain resilience, and the Budget reflects this by introducing new schemes, strengthening liquidity frameworks, and expanding professional support. […]

Budget 2026: Key Changes in Income Tax

Introduction On February 1, 2026, Finance Minister Nirmala Sitharaman presented the Union Budget for the financial year 2026-27. This Budget introduced landmark reforms in direct taxation, focusing on simplification, rationalisation of tax rates, reduction of litigation, and incentivisation of investment. The centrepiece of these reforms is the Income Tax Act, 2025, which will replace the […]

Tobacco Goods- GST to be paid on RSP from Feb 1, 2026

Introduction On January 23, 2026, the Goods and Services Tax Network (GSTN) released an important advisory regarding the reporting of taxable value and tax liability under Retail Sale Price (RSP)-based valuation for notified tobacco goods. This update is highly relevant for businesses engaged in the supply of tobacco products, as it directly impacts how invoices, […]

GST Reforms 2025: Part II

Introduction 2025 has truly been a turning point for GST in India. A host of reforms were introduced to make the system simpler, more equitable, and easier to navigate. From rationalising tax rates on essential goods to fixing inverted duty structures and easing compliance for businesses, these changes have touched households, MSMEs, and professionals alike. […]

Income Tax Act, 2025: A Simplified Tax Era

Introduction For more than six decades, India’s taxation framework was governed by the Income Tax Act, 1961. While it was a landmark law in its time, the Act became increasingly complex due to thousands of amendments, scattered provisions, and archaic language. Taxpayers, professionals, and businesses often struggled to interpret its dense legal text, leading to […]

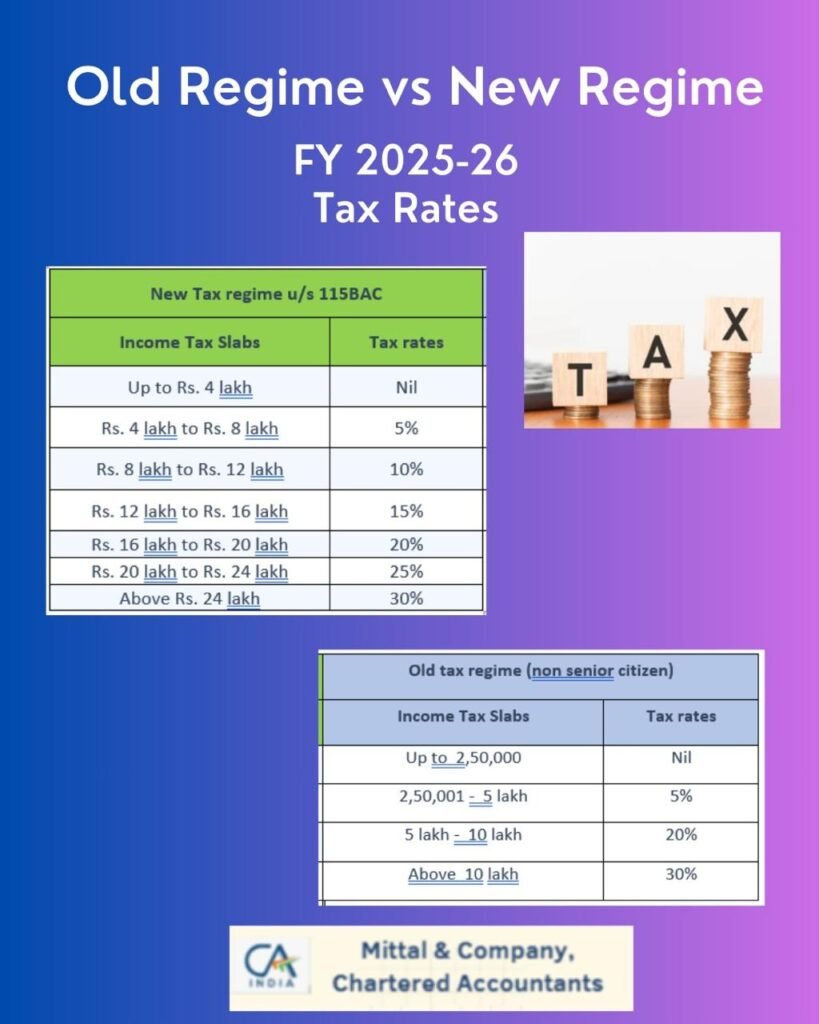

Old Regime vs New Regime u/s 115BAC – FY 2025-26 (AY 2026-27): Which Income Tax Regime Should You Choose?

Introduction: As FY 2025-26 nears its end, taxpayers face a critical phase where accurate TDS deductions, advance tax payments, and final submission of tax declarations to their employer companies must be completed without error. At this juncture, the choice between the Old Tax Regime and the New Tax Regime becomes decisive, as it directly influences […]